MP Econ Issue 4: The Chinese Economy in 2025

Dear readers,

In this special issue, we are making available to all subscribers an excerpt of my economic forecast of China's next five years, part of MacroPolo's “Forecast 2025: China Adjusts Course” report.

In the following excerpt, I make the call that contrary to current expectations, the Chinese economy will actually become more open as a result of intensifying external pressures. The first test of that key call came today in the readout of the just-concluded Communist Party Fifth Plenum, which released the broad contours of the 14th Five-Year Plan (2021-2025) and offered Beijing’s long-term vision through 2035.

In the plan, the theme of openness appears to have received the kind of prominence that it did not enjoy in Beijing’s original 2035 goals announced in 2017. Similarly, there are more ambitious and concrete openness goals in the 14th FYP. Moreover, Beijing also explicitly acknowledged the need to stabilize China’s external environment, a line that did not appear in the 13th FYP readout. The following forecast first establishes my base case, then explains in detail why and how the Chinese economy will likely become more open.

Base Case (70%)

From the vantage point of 2020, the Chinese economy is under considerable strain, both externally and internally. First, China has bungled its relationship with a number of G20 economies that have repercussions for market access. Second, China faces a slew of legacy problems and secular trends that constrain growth, ranging from local debt and an aging population to a less competitive business environment.

These challenges are not intractable, but overcoming them will require Beijing to adapt its current approach to managing both the external environment and domestic reforms. Skepticism abound over the prospects of reform, but our base case is one in which China reforms its way out of current challenges.

This certainly seems at odds with present trends, but it is premised on Beijing’s renewed emphasis on economic security as a result of its assessment of the external environment. That is the single most important variable that has changed significantly over the last few years and that will remain challenging for the foreseeable future. Yet it is precisely because of this pressure that the prospect of meaningful changes in the Chinese economy is more likely than it has been in nearly a decade.

These changes center on three key issues: 1) further openings to foreign investment to stabilize the external environment; 2) domestic reforms to improve the business climate; and 3) prioritizing the expansion of the middle class to bolster domestic consumption. In fact, these will likely be the defining themes in the 14th FYP that takes China through 2025 and that will set a foundation for the next two FYPs through 2035, a crucial year for meeting Xi Jinping’s national rejuvenation objective.

More Openness to Stabilize External Environment

For all the talk of China’s inward turn, it actually remains a relatively open economy, which means that it is especially sensitive to volatility in the external environment (see Figure 1). The Chinese economy still depends on global markets for demand, technologies, and capital. Yet it is currently facing a confluence of factors: anemic global economic recovery as a result of the pandemic, the rapid deterioration in market access of advanced economies, and continued decoupling of technology supply chains.

Figure 1. Exports Matter Much More to China Than To the US (% of GDP)

Source: Wind.

The search for organic demand isn’t exclusive to China, and it should be able to withstand the near-term impact on exports. More crucial over the next few years is China’s access to markets and technology, which are becoming constrained as tensions with the United States and other major economies mount. Since value-added manufacturing and technology sectors are integral to China’s future economic development, current dynamics, if left unattended, could seriously dampen that future. This would in turn undermine Xi’s “national rejuvenation” objective, which is largely defined in economic terms.

Beijing’s latest concept of “internal circulation” has been interpreted as its attempt to offset external volatility by closing itself off. But that would be disastrous for the economy. For example, Huawei has recently admitted that Washington’s latest ban has effectively crippled its development of advanced chips. Moreover, when it comes to cross-border financial transactions, China will continue to rely on the SWIFT system, which cannot be replaced by a domestic alternative.

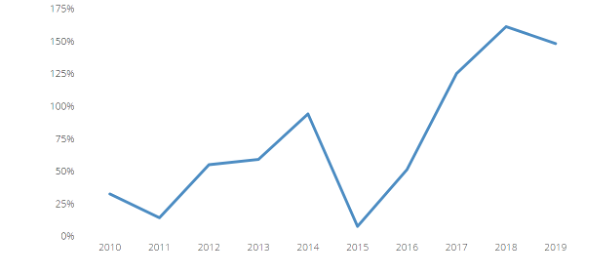

Even if China can achieve marginally more technology independence over the next five years (see technology base case), it simply cannot quit global capital. This is because China is increasingly reliant on foreign portfolio inflows to balance its financial account (see Figure 2). If foreign capital senses that China is untethering itself from global markets, capital inflows will quickly dry up as investors swiftly exit. Capital flight of such proportions would create a currency crisis that dwarfs the 2015-2016 episode. These considerations impose limits on the extent of Beijing’s inward turn.

Figure 2. China Is Increasingly Reliant on Foreign Portfolio Inflows ($ billio

Source: State Administration of Foreign Exchange.

Instead, Beijing will likely respond by making the China market much more open in order to prevent what could become a wholesale isolation of the Chinese economy. Although cognizant of the fact that a return to the old normal before 2016 isn’t likely, Beijing’s wants to arrest the rapid deterioration in the external environment. A stable external environment was a necessary ingredient in China’s remarkable growth over three decades and the main purpose of Deng’s “hide and bide” principle.

Embracing FDI can help China build significant foreign stakeholders in the Chinese economy that can serve as a counterweight to conflicts in other geopolitical arenas that are less amenable to immediate solutions. This is likely a reason behind accelerated talks on a possible EU-China investment treaty.

While Beijing may well be relearning some of Deng’s lessons, China is also learning its own lessons on the long-term cost of protectionism. In sectors such as financial services and automotive, instead of nurturing globally competitive firms, protectionism has instead led to rampant rent-seeking and resulted in less competitive industries. Curtailing the negative effects of protectionism was likely a key reason behind Beijing’s decision to further open both the financial services and the auto sectors, even amid the US-China trade war.

Openness, on the other hand, has been a crucial contributor to competitiveness in the Chinese economy. In many sectors, companies tend to rely more on their incumbency and local protection, rather than innovation, to maintain their market share. Foreign competition can bring that needed “gaiatsu” (foreign pressure) to raise the game of domestic firms and create a more competitive environment overall. Therefore, the push for openness is more aligned with domestic considerations and serves China’s own interest, making it more likely in the current environment.

Since protection of domestic firms has been a major source of unfair competition, the State Council has already rolled out policies for creating a more level playing field, emphasizing the protection of intellectual property. Beijing wants Chinese firms to catch up with the global frontier, and openness predicated on fair competition is the only way to credibly do so. The market entry of Tesla as a wholly foreign-owned enterprise fits with this approach.